{kind=link}

UBO verification—short for Ultimate Beneficial Owner verification—is a core financial crime compliance process used to identify, verify, and continuously monitor the real natural persons who ultimately own, control, or exert decisive influence over a legal entity, regardless of how many intermediary companies, trusts, partnerships, or nominee arrangements sit between the individual and the business. In regulated financial, fintech, payments, crypto, lending, and B2B infrastructure environments, UBO verification exists to eliminate opacity in corporate ownership structures by forcing transparency down to the human level. It ensures that institutions do not unknowingly provide services to shell companies, front entities, or complex ownership vehicles designed to conceal money laundering, terrorism financing, sanctions evasion, tax crimes, corruption, or politically exposed influence. At a systems level, UBO verification transforms abstract legal entities into attributable, risk-assessable human actors, enabling institutions to assign accountability, apply risk controls, and satisfy global AML, CFT, and regulatory disclosure obligations with defensible evidence rather than assumptions.

One-Sentence Definition of UBO Verification

UBO verification is the compliance process of identifying, validating, and documenting the real natural persons who ultimately own, control, or significantly influence a legal entity, in order to assess financial crime risk and meet regulatory AML and KYB obligations.

What Is UBO Verification (Ultimate Beneficial Owner Verification)

What “Ultimate Beneficial Owner” Means in Compliance Terms

In regulatory and compliance language, an Ultimate Beneficial Owner (UBO) is not the company itself, not its directors on paper, and not necessarily the shareholders listed on the first ownership layer. Instead, a UBO is the real human being who ultimately benefits from, controls, or influences the entity’s activities, even if that control is exercised indirectly, informally, or through layered legal structures. Regulators intentionally define UBOs broadly to prevent abuse of corporate complexity as a shield against accountability. In practice, UBO determination requires institutions to look beyond surface-level registrations and follow ownership and control chains until a living individual is identified or conclusively ruled out.

From a strict compliance perspective, a person qualifies as a UBO when one or more of the following conditions are met:

- Ownership-based control

- Direct or indirect ownership of a defined percentage of shares or equity (commonly 25%+, but jurisdiction-dependent)

- Beneficial entitlement to profits, dividends, or residual value

- Control-based influence

- Ability to appoint or remove directors or senior management

- Veto rights, casting votes, or contractual control mechanisms

- Operational or de facto control

- Exercising dominant influence without formal ownership

- Acting through nominees, proxies, or informal arrangements

- Fallback identification rules

- When no individual meets ownership thresholds, senior managing officials may be treated as UBOs for disclosure purposes

Crucially, UBO status is about reality, not paperwork. Compliance frameworks prioritize substance over form, meaning that even if an individual’s name never appears on a registry, they may still be classified as a UBO if evidence shows they ultimately benefit from or control the entity.

What UBO Verification Actually Verifies (Ownership, Control, Influence)

UBO verification is often misunderstood as a simple shareholder check. In reality, it is a multi-dimensional verification process that validates three distinct but interrelated dimensions: ownership, control, and influence. Each dimension addresses a different method by which financial crime risk can be hidden inside corporate structures, and effective UBO verification must cover all three to be regulatorily defensible.

1. Ownership verification focuses on economic reality and answers the question: Who ultimately owns the business?

This includes:

- Mapping direct and indirect shareholding chains

- Tracing ownership through holding companies, LLPs, trusts, and SPVs

- Calculating cumulative ownership percentages across multiple layers

- Identifying beneficial entitlement even when shares are held by intermediaries

2. Control verification addresses governance power and answers the question: Who can make decisions?

This involves:

- Reviewing voting rights and shareholder agreements

- Identifying individuals with board appointment or removal powers

- Analyzing management control structures

- Detecting contractual or negative control arrangements

3. Influence verification captures hidden or informal power and answers the question: Who truly calls the shots?

This requires:

- Assessing nominee relationships and proxy arrangements

- Identifying individuals providing decisive funding or guarantees

- Reviewing beneficial relationships not reflected in formal documents

- Evaluating de facto controllers acting behind the scenes

To complete UBO verification, institutions must identify, verify identity, and document evidence for each qualifying individual using reliable, independent sources. This typically includes government-issued identity documents, registry confirmations, ownership charts, declarations, and risk screening outputs. The objective is not merely to name a UBO, but to create an auditable, regulator-ready record proving how and why that individual was classified as such.

Where UBO Verification Sits Within KYB and AML Frameworks

UBO verification is not a standalone compliance activity; it is a foundational control layer embedded within broader Know Your Business (KYB) and Anti-Money Laundering (AML) frameworks. Its position within these systems is critical because every downstream risk assessment assumes that UBO identification has been performed correctly. If UBO verification fails, the integrity of the entire compliance program is compromised.

Within KYB, UBO verification typically occurs after legal entity existence is confirmed but before risk scoring and onboarding approval. The logical sequence is deliberate:

- Legal entity verification confirms the business exists

- Ownership and control mapping identifies who stands behind it

- UBO verification attributes that structure to real individuals

- Risk profiling evaluates exposure based on those individuals’ profiles

Within AML, UBO verification enables:

- Sanctions screening at the human level

- Politically Exposed Person (PEP) identification

- Adverse media and reputation risk assessment

- Ongoing monitoring when ownership or control changes

From a systems perspective, UBO verification acts as the bridge between corporate compliance and individual risk assessment. AML rules apply to people, not abstractions, and UBO verification is the mechanism that translates a company into the set of humans regulators actually care about. This is why regulators globally treat deficient UBO identification as a serious compliance failure, often citing it as a root cause in enforcement actions, fines, and license revocations.

In mature compliance architectures, UBO verification is therefore continuous rather than static, integrated into onboarding, periodic reviews, event-driven updates, and transaction monitoring triggers. It ensures that institutions always know who they are really doing business with, even when ownership structures evolve over time.

What UBO Verification Is NOT

This section exists to eliminate ambiguity, dismantle common misconceptions, and draw hard boundaries around what UBO verification does not represent in regulated financial, fintech, payments, crypto, lending, and B2B infrastructure environments. High-ranking pages fail here because they blur UBO verification with adjacent controls such as company lookup, director KYC, or static onboarding checks. Search engines reward clarity at the exclusion layer. The purpose of this section is to remove false equivalence and explicitly define the limits of UBO verification so that its true scope, depth, and operational intent are unmistakable.

UBO verification is not basic company registration checks

UBO verification must never be confused with simple company registration validation, registry lookups, or incorporation status checks. While company registration data is often an input into UBO workflows, it is fundamentally insufficient to establish ultimate ownership, control, or economic interest.

Basic company registration checks typically answer only surface-level questions, such as:

- Whether a legal entity exists

- Whether it is active, dissolved, or struck off

- Its incorporation date and jurisdiction

- Its registered address

- Its directors or officers as filed with a registry

These checks stop at the entity layer. UBO verification, by contrast, operates at the control and economic reality layer, which company registries were never designed to fully represent.

Key distinctions that make this difference critical:

- Registries reflect legal form, not economic truth

Many jurisdictions allow nominee directors, nominee shareholders, bearer instruments (historically), and intermediary holding vehicles. Registry data may show who appears to own or manage the company, not who ultimately benefits from it. - Ownership chains are rarely flat

UBO verification must traverse multi-layered ownership structures involving:- Parent companies

- Subsidiaries

- Holding entities

- Trusts and foundations

- Offshore or cross-border vehicles

- Threshold-based ownership is ignored by simple checks

UBO frameworks require identification of individuals who meet ownership or control thresholds (commonly 10%, 25%, or equivalent voting/control rights). Company registration data does not compute or enforce these thresholds. - Control is not always equity-based

UBO verification evaluates:- Voting agreements

- Shareholder agreements

- Veto rights

- Board control

- Power of attorney

- De facto influence

- Regulatory intent is absent from registration systems

Registries exist to record entities, not to prevent money laundering, terrorism financing, sanctions evasion, or financial crime. UBO verification exists specifically to satisfy AML, CFT, and sanctions obligations defined by bodies such as Financial Action Task Force and enforced by regulators like FinCEN.

In short, company registration checks confirm that a business exists.

UBO verification determines who truly controls and economically benefits from that business, even when the answer is intentionally obscured.

UBO verification is not KYC for directors only

Another common and damaging misconception is treating UBO verification as a narrow extension of director KYC. While director identification may form one component of an ownership assessment, equating the two creates material compliance blind spots.

Director KYC focuses on appointed individuals with managerial authority. UBO verification focuses on natural persons with ultimate ownership or control, regardless of whether they hold an official title.

Why director-only KYC fails as a substitute for UBO verification:

- Directors are often professional or nominee roles

In many jurisdictions, directors may be:- Corporate service providers

- Local compliance nominees

- Professional board members

- Temporary appointees

- Owners frequently remain off-record

True beneficial owners may:- Hold shares indirectly

- Control entities through trusts or partnerships

- Exert influence via contractual rights

- Remain deliberately invisible to public filings

- Ownership and control are distinct risk dimensions

UBO verification explicitly evaluates:- Equity ownership

- Voting power

- Economic entitlement

- Control through other means

- Regulatory definitions explicitly reject director-only identification

AML and CFT regulations worldwide define UBOs as natural persons who ultimately own or control a customer, not merely those who manage day-to-day operations. - Sanctions and PEP exposure often sits above the director layer

High-risk exposure frequently resides with:- Silent partners

- Foreign principals

- Politically exposed individuals

- Shadow controllers

- Sanctions breaches

- Undisclosed PEP risk

- Regulatory enforcement actions

- Director turnover does not equal ownership change

Directors can be replaced quickly. UBOs tend to remain stable over longer horizons. Treating director KYC as UBO verification causes institutions to misinterpret continuity of risk.

A precise way to frame the distinction:

- Director KYC answers: “Who runs the company operationally?”

- UBO verification answers: “Who ultimately owns, controls, or profits from the company?”

They solve different problems, address different risks, and satisfy different regulatory expectations.

UBO verification is not a one-time onboarding task

Perhaps the most operationally dangerous misconception is treating UBO verification as a static, check-the-box activity performed once during onboarding. Modern regulatory expectations explicitly reject this model.

UBO verification is a continuous risk control, not a single event.

Why one-time UBO checks are insufficient:

- Ownership structures change over time

Businesses evolve through:- New funding rounds

- Share transfers

- Mergers and acquisitions

- Management buyouts

- Silent ownership reallocations

- Control can shift without registry updates

Changes in:- Voting agreements

- Shareholder rights

- Control provisions

- Informal influence

- Risk profiles are dynamic

A UBO may:- Become sanctioned

- Enter PEP status

- Be added to adverse media

- Appear in enforcement actions

- Regulators increasingly expect ongoing monitoring

Supervisory guidance now emphasizes:- Periodic refresh cycles

- Event-driven reviews

- Trigger-based reassessments

- Continuous sanctions and PEP screening

- Transaction behavior may surface hidden ownership risk

Unusual transaction patterns, cross-border flows, or counterparties may signal:- Undisclosed controllers

- Beneficial owners not declared at onboarding

- Fronting or proxy arrangements

- Lifecycle compliance extends beyond onboarding

UBO verification must persist across:- Account maintenance

- Product expansion

- Credit limit changes

- Geographic expansion

- Regulatory reclassification

A correct operational framing is:

- Onboarding UBO verification establishes a baseline

- Ongoing UBO monitoring preserves accuracy and regulatory defensibility

Institutions that treat UBO verification as a one-time task expose themselves to enforcement risk, audit failures, and systemic blind spots that regulators increasingly penalize.

In summary, UBO verification is not a registry lookup, not director-only KYC, and not a static onboarding exercise. It is a living, ownership-centric, risk-driven control system designed to surface the true natural persons behind legal entities—continuously, defensibly, and in alignment with modern AML and financial crime expectations.

Why UBO Verification Is Important in Financial Services

Hidden ownership as a financial crime risk

Hidden ownership is one of the most persistent and structurally dangerous risk vectors in modern financial systems, because financial crime does not originate at the transaction layer—it originates at the ownership and control layer. When the true Ultimate Beneficial Owner (UBO) of an entity is obscured through nominee directors, shell companies, layered holding structures, trusts, offshore vehicles, or informal control arrangements, the financial institution loses visibility into who ultimately benefits, who ultimately controls decision-making, and who ultimately bears accountability. This lack of visibility creates a systemic blind spot that is routinely exploited for money laundering, terrorist financing, sanctions evasion, tax evasion, fraud, insider trading, corruption, and proceeds-of-crime recycling.

From a risk mechanics perspective, hidden ownership enables criminals to separate economic benefit from legal responsibility, which undermines every downstream compliance control. Transactions may appear benign when assessed against the immediate counterparty, but become high-risk once traced to the concealed beneficial owner behind the entity.

Key ways hidden ownership elevates financial crime risk include:

- Money laundering through corporate layering

- Criminals use multi-jurisdictional ownership chains to distance illicit funds from their origin

- Each layer adds opacity, delays investigations, and increases enforcement complexity

- Shell entities often have no operating activity, employees, or physical presence

- Sanctions and embargo circumvention

- Sanctioned individuals or entities hide behind minority stakes, proxy shareholders, or family members

- Control may be exercised without meeting simplistic percentage-based thresholds

- Payments routed through unsanctioned intermediaries mask ultimate exposure

- Terrorist financing and organized crime facilitation

- Front companies provide legitimate-looking access to the financial system

- Small, repeated transactions evade basic transaction monitoring without ownership context

- Profits are funneled back to prohibited actors through dividends, loans, or management fees

- Fraud and insider abuse

- Related-party transactions are concealed through undisclosed ownership links

- Entities controlled by the same UBO transact with each other to manipulate pricing or move funds

- Financial institutions become unwitting facilitators of self-dealing schemes

Without UBO verification, institutions are effectively assessing entities in isolation, rather than as extensions of the individuals who control them. This creates false confidence, underestimates risk, and allows sophisticated criminal networks to exploit regulatory arbitrage at scale. In practical terms, hidden ownership converts regulated financial infrastructure into a conduit for illicit activity, not because controls are absent, but because they are applied at the wrong layer.

Regulatory obligations and enforcement pressure

Regulatory frameworks across jurisdictions increasingly recognize that UBO verification is not optional, interpretive, or discretionary—it is a foundational compliance obligation embedded into AML, CFT, KYC, and KYB regimes. Regulators no longer accept surface-level identification of legal entities; they require financial institutions to demonstrate reasonable certainty about who ultimately owns or controls a customer, and to prove that this information is accurate, current, and risk-assessed.

Global enforcement trends show a clear shift from rule-based compliance to outcome-based accountability, where failures in UBO identification are treated as governance failures, not technical oversights.

Key regulatory drivers intensifying UBO enforcement include:

- Expanded AML and CFT mandates

- Institutions must identify beneficial owners above defined ownership or control thresholds

- Control is assessed not only through equity, but through voting rights, influence, and contractual power

- Ongoing monitoring is required, not just onboarding-time checks

- Severe financial penalties and supervisory actions

- Multi-million and billion-dollar fines linked directly to beneficial ownership failures

- License restrictions, consent orders, and business activity caps imposed by regulators

- Mandatory remediation programs with independent monitors

- Personal accountability of senior management

- Boards and compliance officers held responsible for systemic UBO failures

- “I didn’t know” is no longer a defensible position under modern enforcement standards

- Governance frameworks must show oversight of ownership risk

- Cross-border regulatory coordination

- Information sharing between regulators reduces jurisdictional blind spots

- Inconsistent UBO practices across regions trigger supervisory scrutiny

- Global institutions must align to the strictest applicable standard, not the weakest

- Beneficial ownership transparency initiatives

- Centralized UBO registries increase regulator expectations of accuracy and verification

- Institutions are expected to reconcile customer-provided data with authoritative sources

- Discrepancies must be investigated, documented, and resolved

Crucially, regulators assess not only whether UBOs are identified, but how well institutions understand and use that information. Weak documentation, outdated ownership data, reliance on self-attestation, or failure to detect changes in control are treated as compliance failures in their own right.

In enforcement actions, regulators repeatedly emphasize that UBO verification is the gateway control: if it fails, every subsequent AML control is compromised. As a result, institutions that underinvest in UBO verification face disproportionate regulatory risk, even if transaction monitoring and reporting appear robust on paper.

Why entity-level risk cannot be assessed without UBOs

Entity-level risk assessment without UBO information is structurally incomplete, because legal entities do not possess intent, ethics, or behavior—people do. Risk resides in the individuals who ultimately control an entity’s decisions, financial flows, and strategic direction. Evaluating an entity without understanding its UBOs is equivalent to assessing credit risk without knowing the borrower, or sanctions risk without knowing the beneficiary.

From a risk architecture standpoint, UBOs are the anchor point that connects disparate risk domains into a coherent profile.

Without UBO identification, institutions cannot reliably assess:

- True risk exposure

- Politically Exposed Persons (PEPs) hidden behind corporate vehicles

- Prior criminal history, regulatory actions, or adverse media linked to owners

- Jurisdictional risk associated with the UBO, not just the registered entity

- Related-party and concentration risk

- Multiple entities controlled by the same UBO treated incorrectly as independent customers

- Aggregated exposure limits breached unknowingly

- Collusion and circular transaction risks missed entirely

- Behavioral and transactional risk

- Transaction patterns make sense only when mapped to the ultimate controller

- Legitimate-looking business activity may mask personal wealth movement

- Sudden changes in transaction behavior often correlate with ownership changes

- Lifecycle and ongoing risk

- Ownership structures evolve through mergers, transfers, inheritance, or informal agreements

- Static entity profiles quickly become outdated without UBO monitoring

- Risk ratings degrade silently over time without ownership refresh

- Exit and reputational risk

- Institutions may be publicly linked to high-risk individuals through undisclosed ownership

- Media exposure often focuses on “who was really behind the company”

- Reputational damage frequently exceeds regulatory penalties

Effective entity-level risk assessment therefore requires UBO data to be:

- Identified with clarity across ownership and control dimensions

- Verified against reliable, independent, and jurisdiction-appropriate sources

- Contextualized within sanctions, PEP, adverse media, and geographic risk frameworks

- Monitored continuously for changes in ownership, control, or influence

In modern financial services, UBO verification is not a compliance checkbox—it is the analytical foundation upon which risk scoring, due diligence depth, monitoring thresholds, and decision-making logic are built. Without UBOs, entity risk assessments are superficial, reactive, and structurally incapable of capturing real exposure. With robust UBO verification, institutions gain the visibility required to assess risk as regulators expect it to be assessed: at the level where control, benefit, and accountability ultimately reside.

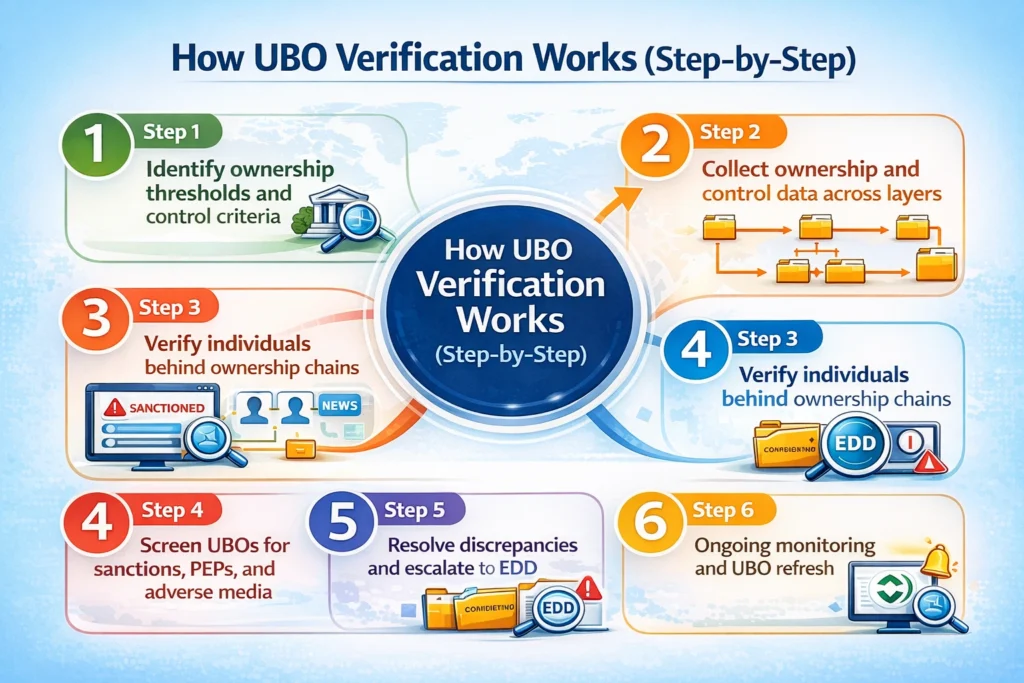

How UBO Verification Works (Step-by-Step)

Ultimate Beneficial Owner (UBO) verification is not a single check, document request, or database lookup. It is a deterministic, evidence-driven, multi-layered workflow designed to identify, validate, and continuously monitor the natural persons who ultimately own or control a legal entity. Properly implemented, UBO verification reduces hidden ownership risk, prevents regulatory breaches, and establishes defensible compliance across AML, CTF, sanctions, and financial crime programs.

The workflow below reflects how production-grade UBO verification systems operate in regulated financial services, fintech infrastructure, payments, crypto platforms, lending, and B2B financial onboarding. Each step is sequential, interdependent, and non-optional. Skipping or weakening any step compromises the integrity of the entire KYB and AML framework.

Step 1: Identify ownership thresholds and control criteria

The first step in UBO verification is to define what qualifies as “beneficial ownership” and “control” for the specific jurisdiction, regulatory regime, and risk profile of the entity being onboarded. This is a foundational scoping exercise that determines who must be identified, verified, screened, and monitored.

Ownership thresholds are not universal. They vary by regulation, country, and sometimes by industry or product risk. Control criteria are even more nuanced, as control may exist without equity ownership.

Key elements established at this stage include:

Ownership thresholds

- Percentage-based ownership cutoffs (commonly 25%, but can be 10% or lower in high-risk scenarios)

- Aggregation rules for indirect ownership across layers

- Treatment of split or dispersed ownership structures

- Rules for joint ownership or acting-in-concert arrangements

Control criteria (non-ownership)

- Board appointment or removal rights

- Voting power disproportionate to equity

- Veto rights over strategic or financial decisions

- Contractual control through shareholder agreements

- Trustee, protector, or settlor authority in trusts

- Senior management roles where no owner meets thresholds

Regulatory alignment

- AML and CFT regulations applicable to the jurisdiction

- Financial Action Task Force (FATF) guidance

- Local corporate registry disclosure requirements

- Sector-specific rules (banking, payments, crypto, securities)

Risk-based adjustments

- Lower thresholds for high-risk jurisdictions

- Expanded control definitions for complex entities

- Enhanced scrutiny for nominee or bearer share exposure

This step answers one critical question with precision:

Who, exactly, must be identified as a UBO under applicable law and risk policy?

Without clear thresholds and control definitions, UBO verification becomes subjective, inconsistent, and indefensible during audits or regulatory reviews.

Step 2: Collect ownership and control data across layers

Once thresholds and control rules are defined, the next step is systematic data collection across the entire ownership and control chain. This is where UBO verification transitions from theory to structural analysis.

Modern business entities rarely have simple, single-layer ownership. Instead, they often involve nested legal entities spanning multiple jurisdictions, each with its own registry standards and disclosure quality.

This step requires constructing a complete ownership map, starting from the onboarding entity and traversing upward until natural persons are reached.

Data collected typically includes:

Entity-level information

- Legal name, registration number, and jurisdiction

- Entity type (LLC, corporation, partnership, trust, foundation)

- Incorporation date and status

- Registered address and operating address

Ownership structure data

- Direct shareholders and ownership percentages

- Intermediate holding companies

- Parent and ultimate parent entities

- Subsidiaries relevant to control or consolidation

Control relationships

- Directors and officers

- Authorized signatories

- Managing partners or general partners

- Trustees, protectors, or fund managers

- Power-of-attorney holders

Supporting documentation

- Corporate registry extracts

- Shareholder registers

- Articles of association and bylaws

- Trust deeds or partnership agreements

- Cap tables and side letters where applicable

Jurisdiction-specific considerations

- Variations in registry transparency

- Delays or gaps in public data availability

- Reliance on certified documents in opaque jurisdictions

The objective at this stage is exhaustiveness, not verification. Every ownership and control relationship must be captured, even if its relevance is not yet clear. Missing a layer here guarantees failure in downstream verification and screening.

Step 3: Verify individuals behind ownership chains

After ownership and control chains are fully mapped, the workflow reaches its most critical transition point: identifying and verifying the natural persons at the end of those chains.

At this stage, legal entities stop being the focus. The objective becomes confirming the real, living individuals who ultimately own or control the business.

This step involves:

Identification of UBOs

- Natural persons exceeding ownership thresholds (direct or indirect)

- Individuals exercising control through non-ownership means

- Senior managing officials when no owner qualifies

Identity data collection

- Full legal name (including aliases and transliterations)

- Date and place of birth

- Nationality and residency

- Government-issued identification numbers

- Residential address history

Identity verification

- Document verification (passport, national ID, driver’s license)

- Biographic data consistency checks

- Registry cross-references where available

- Liveness or biometric checks in digital onboarding

Ownership attribution validation

- Mathematical confirmation of indirect ownership percentages

- Chain-of-ownership calculations across entities

- Validation of control claims against legal documents

Edge case handling

- Nominee shareholders acting on behalf of principals

- Bearer share exposure

- Trust beneficiaries with contingent interests

- Complex fund or SPV structures

This step transforms abstract corporate structures into accountable human identities. Errors here create direct regulatory exposure, including AML violations, sanctions breaches, and misreporting of beneficial ownership.

Step 4: Screen UBOs for sanctions, PEPs, and adverse media

Once UBO identities are verified, each individual must be assessed for financial crime, political exposure, and reputational risk. This step determines whether onboarding can proceed, requires enhanced controls, or must be rejected outright.

Screening is not a one-time checkbox. It is a probabilistic risk assessment based on multiple data sources and contextual interpretation.

Core screening dimensions include:

Sanctions screening

- Global sanctions lists (OFAC, EU, UN, UK, etc.)

- Country-specific and sectoral sanctions

- Ownership-based sanctions exposure (50% rule)

- Secondary sanctions implications

Politically Exposed Person (PEP) screening

- Domestic PEPs

- Foreign PEPs

- International organization officials

- Family members and close associates

- Historical PEP status with cooling-off considerations

Adverse media screening

- Financial crime allegations

- Fraud, corruption, bribery, and embezzlement

- Regulatory enforcement actions

- Litigation and civil judgments

- Association with criminal enterprises

Risk scoring and context

- Severity and recency of findings

- Jurisdictional risk amplification

- Relevance to business activities

- Source credibility and corroboration

Outputs of this step typically include:

- Clean clearance

- Low-risk flag with monitoring

- High-risk flag requiring escalation

- Hard stop due to sanctions or prohibitions

This stage converts identity into risk intelligence, enabling defensible onboarding decisions aligned with AML and CFT obligations.

Step 5: Resolve discrepancies and escalate to EDD

UBO verification rarely produces perfectly clean results. Discrepancies, ambiguities, and conflicts are expected, particularly in complex or high-risk structures. This step is where human judgment, documented reasoning, and enhanced due diligence (EDD) become essential.

Common discrepancies include:

- Ownership percentages that do not sum correctly

- Conflicting registry data across jurisdictions

- Mismatched names, dates, or addresses

- Undisclosed control relationships

- Media allegations without legal outcomes

Resolution activities involve:

Discrepancy analysis

- Root cause identification

- Cross-source reconciliation

- Temporal analysis of changes in ownership

Additional evidence collection

- Certified documents

- Legal opinions or attestations

- Source-of-wealth and source-of-funds explanations

- Management interviews or declarations

Enhanced Due Diligence (EDD) triggers

- High-risk jurisdictions

- PEP involvement

- Adverse media with credible sources

- Complex or opaque ownership chains

Decision documentation

- Risk rationale and justification

- Mitigating controls applied

- Approval or rejection rationale

- Audit-ready records

This step ensures that unresolved uncertainty is explicitly addressed, not ignored. Regulators expect to see how ambiguity was handled, not just that data was collected.

Step 6: Ongoing monitoring and UBO refresh

UBO verification does not end at onboarding. Ownership and control are dynamic, and regulatory expectations require continuous accuracy over time, not just point-in-time compliance.

Ongoing monitoring ensures that UBO data remains current and risk exposure is promptly identified.

Key components include:

Trigger-based monitoring

- Ownership changes

- Director or officer updates

- Corporate restructuring events

- Mergers, acquisitions, or divestitures

Periodic refresh cycles

- Scheduled UBO re-verification

- Document updates

- Reconfirmation of control roles

Continuous screening

- Real-time sanctions updates

- PEP status changes

- New adverse media coverage

Risk reassessment

- Changes in jurisdictional risk

- Product or transaction behavior shifts

- Regulatory updates affecting thresholds or definitions

Governance and auditability

- Versioned ownership records

- Change logs and timestamps

- Evidence retention

- Regulatory reporting readiness

This final step transforms UBO verification from a static compliance task into a living risk management system, aligned with modern AML, KYB, and financial crime prevention expectations.

Taken together, these six steps represent a complete, regulator-grade UBO verification lifecycle. Each step is equally critical. Weakness in any single stage undermines the integrity of the entire system, increases financial crime exposure, and erodes regulatory defensibility.

Benefits of Automated UBO Verification

Speed and scalability

Automated Ultimate Beneficial Owner (UBO) verification fundamentally transforms the speed at which regulated institutions can establish ownership transparency, assess control, and make onboarding or risk decisions. Unlike manual workflows—where verification is constrained by analyst availability, document turnaround times, and jurisdiction-specific research—automation introduces near-real-time execution at scale, without proportional increases in cost or headcount.

At a system level, speed in automated UBO verification is not merely about faster processing; it is about parallelization of verification logic across multiple data layers simultaneously. An automated UBO engine can ingest corporate registry data, shareholder filings, beneficial ownership disclosures, sanctions lists, adverse media feeds, and control indicators in parallel, producing a consolidated ownership map within minutes rather than days or weeks.

Key dimensions of speed and scalability include:

- Instant entity resolution

- Automated systems resolve entity identifiers (company name variants, registration numbers, LEIs, tax IDs) in milliseconds.

- Fuzzy matching and deterministic rules eliminate delays caused by spelling differences, transliteration issues, or formatting inconsistencies.

- Concurrent ownership traversal

- Multi-layer ownership chains—parent companies, intermediate holding entities, trusts, foundations, and nominee structures—are traversed algorithmically.

- Ownership thresholds (e.g., 10%, 25%, control-based triggers) are calculated dynamically across hundreds or thousands of nodes.

- Elastic scalability

- Automated UBO platforms scale horizontally, allowing institutions to process:

- Thousands of KYB files per day

- Bulk periodic reviews

- Sudden onboarding spikes during product launches or geographic expansion

- Performance does not degrade with volume, unlike analyst-driven workflows.

- Automated UBO platforms scale horizontally, allowing institutions to process:

- Continuous availability

- Automated verification operates 24/7 across time zones.

- There is no dependency on regional teams or business hours, which is critical for global fintechs, crypto platforms, and cross-border payment providers.

From a commercial and operational perspective, scalability directly supports:

- High-growth fintech onboarding

- Embedded finance programs

- Marketplace and platform-based business models

- Global B2B payments and treasury infrastructure

In practice, automation enables institutions to decouple growth from compliance bottlenecks, ensuring that UBO verification does not become a gating constraint as transaction volume, customer count, or jurisdictional exposure increases.

Reduced human error and inconsistency

Manual UBO verification is inherently vulnerable to human error due to its reliance on subjective judgment, fragmented data interpretation, and repetitive investigative tasks. Automated UBO verification mitigates these risks by enforcing deterministic logic, standardized rulesets, and repeatable workflows, dramatically improving accuracy and consistency across the organization.

Human-driven verification introduces multiple failure points:

- Misinterpretation of ownership documents

- Inconsistent application of ownership thresholds

- Fatigue-driven oversight during high-volume reviews

- Variability between analysts, teams, and regions

Automation addresses these issues through system-enforced precision.

Core mechanisms by which automation reduces error and inconsistency include:

- Rule-based ownership determination

- Ownership percentages are calculated mathematically, not estimated.

- Control indicators (voting rights, board control, veto powers) are applied uniformly.

- Standardized decision logic

- The same UBO rules apply regardless of:

- Jurisdiction

- Customer size

- Analyst seniority

- This eliminates discrepancies between similar cases handled by different teams.

- The same UBO rules apply regardless of:

- Automated document validation

- System checks ensure documents are:

- Current

- Authentic

- Jurisdictionally valid

- Expired, incomplete, or mismatched records are flagged automatically.

- System checks ensure documents are:

- Elimination of transcription errors

- Data ingestion is machine-to-machine where possible, reducing:

- Manual data entry mistakes

- Copy-paste errors

- Mislabeling of individuals or entities

- Data ingestion is machine-to-machine where possible, reducing:

Beyond pure accuracy, consistency is critical for defensibility. Regulators and auditors assess not only whether a firm reached the “right” conclusion, but whether it applied the same standards across all customers. Automated UBO verification ensures that:

- Similar ownership structures yield similar outcomes

- Edge cases are handled predictably

- Exceptions are logged, justified, and traceable

This consistency is particularly important for institutions operating across multiple jurisdictions, where local teams might otherwise interpret global policies differently. Automation enforces a single source of truth for UBO determination, reducing internal friction and compliance risk.

Improved auditability and regulatory confidence

One of the most significant advantages of automated UBO verification is the creation of comprehensive, immutable, and regulator-ready audit trails. In contrast to manual processes—where decision rationale may be scattered across emails, spreadsheets, and analyst notes—automation produces structured evidence that can be reviewed, reproduced, and defended.

Regulatory expectations around UBO verification extend beyond identification; they require firms to demonstrate how and why a particular individual was determined to be (or not be) a beneficial owner. Automated systems are designed to meet this expectation by default.

Key auditability and regulatory confidence benefits include:

- End-to-end decision traceability

- Every step in the UBO determination process is logged:

- Data sources queried

- Ownership percentages calculated

- Thresholds applied

- Risk flags triggered

- This creates a complete decision lineage.

- Every step in the UBO determination process is logged:

- Time-stamped evidence

- Automated systems capture:

- When data was accessed

- When ownership was verified

- When reviews or escalations occurred

- This is critical for demonstrating compliance at a specific point in time.

- Automated systems capture:

- Versioned ownership snapshots

- Ownership structures are preserved as historical records.

- Institutions can show:

- What ownership looked like at onboarding

- How it evolved over time

- When changes triggered reviews or alerts

- Regulator-aligned reporting

- Automated platforms generate reports aligned with:

- AML regulations

- KYB requirements

- Beneficial ownership disclosure laws

- Reports are standardized, complete, and easy to interpret.

- Automated platforms generate reports aligned with:

From a supervisory standpoint, automation signals institutional maturity. Regulators place higher confidence in firms that can demonstrate:

- Systematic application of UBO rules

- Ongoing monitoring rather than point-in-time checks

- Clear escalation and remediation pathways

As regulatory scrutiny intensifies—particularly around shell companies, complex corporate structures, and cross-border financial crime—automated UBO verification becomes not just an efficiency tool, but a trust-building mechanism between institutions and regulators.

Challenges of Manual UBO Verification

Complex ownership structures

Manual UBO verification struggles most acutely when faced with multi-layered, non-linear ownership structures. Modern corporate ownership rarely follows simple, direct shareholding models; instead, it often involves nested entities, indirect control mechanisms, and jurisdiction-specific legal constructs that are difficult to analyze without automation.

Common complexity drivers include:

- Multi-tier holding companies

- Circular ownership arrangements

- Trusts, foundations, and special purpose vehicles

- Nominee shareholders and bearer structures

- Control exercised through voting agreements rather than equity

In a manual process, analysts must:

- Collect documents from multiple registries

- Interpret varying legal definitions of ownership and control

- Manually calculate indirect ownership percentages across layers

- Determine whether control exists without clear equity thresholds

These tasks are not only time-consuming but cognitively demanding. As ownership depth increases, the probability of oversight increases exponentially. Analysts may miss:

- Hidden control exercised through minority stakes

- Beneficial owners obscured behind legal entities

- Changes in ownership not reflected in outdated documents

Furthermore, manual processes lack the ability to dynamically recompute ownership when new information emerges. A single upstream change can invalidate an entire ownership assessment, requiring full re-analysis.

In practice, this leads to:

- Incomplete UBO identification

- Over-reliance on customer attestations

- Increased regulatory exposure in high-risk cases

Cross-border data opacity

Manual UBO verification becomes particularly fragile in cross-border contexts, where data availability, quality, and accessibility vary widely. Corporate transparency standards differ significantly between jurisdictions, creating information asymmetry that manual teams struggle to overcome.

Challenges include:

- Limited or non-digital corporate registries

- Language barriers and transliteration issues

- Inconsistent disclosure requirements

- Delays in accessing foreign records

- Reliance on unofficial or secondary sources

Manual analysts must often piece together fragmented data from:

- Local registries

- Legal filings

- Third-party reports

- Customer-provided documents

This process is slow and error-prone, and it frequently results in partial visibility rather than full ownership clarity. In some jurisdictions, beneficial ownership data may be legally unavailable, forcing analysts to rely on inference rather than evidence.

Cross-border opacity also complicates:

- Sanctions screening

- Politically exposed person (PEP) identification

- Adverse media correlation

Without automated aggregation and normalization of global data sources, manual teams operate with structural blind spots, increasing exposure to financial crime risk and regulatory criticism.

High operational cost and error risk

Manual UBO verification is one of the most resource-intensive components of compliance operations. It requires highly trained analysts, legal interpretation skills, and significant time investment per case—costs that scale linearly with volume.

Primary cost drivers include:

- Analyst headcount growth

- Ongoing training and policy updates

- External data and registry access fees

- Escalation and rework due to errors

As volume increases, institutions face a trade-off between speed and quality. Rushing manual reviews increases error rates, while maintaining quality slows onboarding and frustrates customers.

Error risk manifests in multiple forms:

- False negatives (missing true beneficial owners)

- False positives (over-flagging low-risk entities)

- Inconsistent decisions across teams

- Inadequate documentation for audits

These errors carry downstream consequences:

- Regulatory fines

- Remediation costs

- Reputational damage

- Customer attrition due to onboarding delays

Ultimately, manual UBO verification creates a fragile compliance model—one that is expensive to maintain, difficult to scale, and increasingly misaligned with modern regulatory and business expectations.

Best Practices for Effective UBO Verification

Effective Ultimate Beneficial Owner (UBO) verification is not achieved through a single tool, database, or compliance checkbox. It is the result of a deliberately engineered control framework that balances regulatory sufficiency, operational scalability, and real-world risk exposure. The most resilient UBO programs are designed as adaptive systems, not static processes. They recognize that ownership structures evolve, control can be exercised without equity, and risk is contextual rather than binary. Best practices therefore focus on how verification decisions are made, why thresholds are applied, and when re-verification is triggered, rather than merely what data is collected. Institutions that follow these practices consistently outperform peers in regulatory outcomes, audit defensibility, and financial crime prevention.

Risk-based ownership thresholds

A risk-based approach to ownership thresholds is foundational to modern UBO verification. While many regulations reference numerical thresholds (such as 25% ownership), effective programs treat these figures as minimum baselines, not absolute truths. Real-world control often exists below formal ownership cutoffs, especially in complex corporate structures, nominee arrangements, trusts, and cross-border entities.

Key principles of risk-based ownership thresholding include:

- Dynamic threshold adjustment based on risk profile

- Lower ownership thresholds (e.g., 10% or even 5%) for:

- High-risk jurisdictions

- Politically Exposed Persons (PEPs)

- Regulated or sensitive industries (crypto, gambling, defense, payments)

- Standard thresholds for low-risk, transparent domestic entities

- Lower ownership thresholds (e.g., 10% or even 5%) for:

- Inclusion of control-based UBOs beyond equity

- Individuals with:

- Voting agreements

- Board appointment rights

- Veto powers

- Management dominance

- Recognition that control can exist without shareholding

- Individuals with:

- Layered ownership look-through logic

- Recursive tracing through:

- Holding companies

- Trusts and foundations

- Partnerships and SPVs

- Identification of natural persons at the terminal layer, not just legal owners

- Recursive tracing through:

- Context-aware aggregation

- Combining indirect holdings across multiple entities

- Identifying concert party arrangements and related-party ownership

Operationally, risk-based thresholds require:

- Clear internal policy documentation explaining why thresholds differ

- Consistent application across onboarding, remediation, and reviews

- Audit-ready rationale for every threshold deviation

This approach aligns UBO verification with risk reality, rather than mechanical compliance, reducing both regulatory exposure and false negatives.

Combining registry data with intelligence sources

Corporate registries are necessary but insufficient for effective UBO verification. They provide legal declarations, not ground truth. Best-in-class programs therefore combine authoritative registry data with independent intelligence sources to detect concealment, misrepresentation, and emerging risk signals.

A multi-source intelligence model typically integrates:

- Official corporate registries

- Company incorporation records

- Shareholding disclosures

- Director and officer listings

- Filing histories and amendments

- Supplementary government datasets

- Sanctions lists

- PEP databases

- Watchlists and enforcement actions

- Court records and insolvency filings

- Commercial intelligence providers

- Beneficial ownership networks

- Adverse media screening

- Corporate linkage analysis

- Historical ownership changes

- Open-source intelligence (OSINT)

- News reporting

- Litigation disclosures

- NGO investigations

- Leaked document databases where legally permissible

Critical best practices when combining sources include:

- Cross-validation, not substitution

- Registry data establishes legal standing

- Intelligence sources test credibility and completeness

- Conflict resolution workflows

- Defined escalation paths when sources disagree

- Analyst-led adjudication supported by documented evidence

- Jurisdictional awareness

- Understanding registry reliability by country

- Compensating for opaque or non-public registries with deeper intelligence

- Temporal analysis

- Tracking ownership changes over time

- Identifying patterns of rapid restructuring or obfuscation

This layered approach transforms UBO verification from a declarative exercise into an evidence-based risk assessment, materially improving detection of hidden beneficial owners and control persons.

Continuous monitoring over static verification

Static, point-in-time UBO verification is structurally incompatible with modern financial risk. Ownership structures, control relationships, and risk profiles evolve continuously, often without triggering formal disclosures. As a result, continuous monitoring is no longer an enhancement; it is a necessity.

Effective continuous UBO monitoring frameworks include:

- Event-driven triggers

- Changes in shareholding or directorship

- New sanctions or PEP designations

- Adverse media emergence

- Jurisdictional risk reclassification

- Periodic reassessment cycles

- Risk-tiered review frequencies:

- High-risk entities: quarterly or event-based

- Medium-risk entities: annual reviews

- Low-risk entities: extended cycles with monitoring overlays

- Risk-tiered review frequencies:

- Automated change detection

- Registry update ingestion

- Corporate network graph updates

- Watchlist delta monitoring

- Human-in-the-loop escalation

- Analysts validate materiality of detected changes

- Decisions documented with rationale and evidence

- Clear ownership of remediation actions

Continuous monitoring delivers several structural advantages:

- Prevents regulatory blind spots between reviews

- Reduces reliance on customer self-disclosure

- Strengthens audit defensibility through demonstrable vigilance

- Aligns compliance posture with real-time risk exposure

Institutions that rely solely on onboarding-time UBO checks are effectively operating with known visibility gaps, a position increasingly indefensible to regulators and counterparties alike.

Key Takeaways

UBO verification is no longer a procedural requirement that can be satisfied through static forms, fixed thresholds, or single-source checks. It has become an inevitable system-level capability for any institution operating in regulated financial, payments, crypto, or B2B ecosystems. The direction of regulation, enforcement, and financial crime sophistication makes this outcome unavoidable rather than optional.

The inevitability is driven by several converging realities:

- Ownership structures are becoming more complex, not simpler

- Control is increasingly exercised through informal or indirect mechanisms

- Regulatory expectations are shifting from rule-following to risk understanding

- Financial crime actors actively exploit static verification models

As a result:

- Risk-based ownership thresholds are no longer advanced practice; they are the minimum viable standard for credible compliance

- Registry-only verification is structurally inadequate in a global, digital economy

- Continuous monitoring is replacing periodic review as the default control model

Organizations that internalize these realities design UBO programs that are:

- Defensible — able to explain not just what was done, but why

- Resilient — capable of adapting as ownership and risk evolve

- Scalable — operationally viable across growth, new markets, and new products

- Future-proof — aligned with where regulatory scrutiny is heading, not where it has been

Conversely, institutions that delay this transition accumulate invisible risk, operational debt, and regulatory exposure that compounds over time. In this context, effective UBO verification is not merely a compliance function. It is an enduring infrastructure layer—one that underpins trust, access to markets, and long-term institutional viability.

Sources:

U.S. Financial Crimes Enforcement Network (FinCEN)

Beneficial Ownership Information Reporting Requirements

https://www.fincen.gov/boi FinCEN.gov

Guidance on Obtaining and Retaining Beneficial Ownership Information

https://www.fincen.gov/resources/statutes-regulations/guidance/guidance-obtaining-and-retaining-beneficial-ownership FinCEN.gov

IRS — Report Beneficial Owner Information

https://www.irs.gov/businesses/report-beneficial-owner-information IRS

Financial Action Task Force (FATF)

FATF Beneficial Ownership Transparency Standards

https://www.fatf-gafi.org/en/topics/beneficial-ownership.html FATF

FATF Guidance on Beneficial Ownership and Transparency of Legal Arrangements

https://www.fatf-gafi.org/en/publications/Fatfrecommendations/Guidance-Beneficial-Ownership-Transparency-Legal-Arrangements.html FATF

Open Government Partnership (Public Registers & Government Commitments)

https://www.opengovpartnership.org/open-gov-guide/anti-corruption-company-beneficial-ownership/ Open Government Partnership

Anti-Money Laundering Framework — France

https://en.wikipedia.org/wiki/Anti%E2%80%93money_laundering_framework_for_financial_institutions_in_France#Customer_knowledge Wikipedia

Last Updated

December 24, 2025

Readers can explore more Fintech Explainers HERE.

Click HERE to explore more.